Silicon Valley's gamble on Trump isn't paying off

Tech stocks have tumbled since Trump took office. More about the mindset that led much of the Valley to support him in the first place.

This was initially supposed to be our paid story for the week, but I'm going to call an audible and leave this free, just because I usually lean that way in the early stages of a major news story that's in Silver Bulletin's purview. And “Liberation Day,” the massive series of tariffs that President Trump announced last week, is the biggest story in the world right now.

It's also the sort of story that I hope can play to our strengths. I'm fascinated by the intersection of politics and markets and the relationship between the presidency and Silicon Valley, which I cover extensively in my book.1

In fact, let's go in the other direction. We're holding a low-key Negative Tariff Sale (this is the only time I'll mention it). Since Trump's tariff rates average 23 percent, you can now get a 23 percent discount on the first year of an annual Silver Bulletin subscription. The offer will expire at market close on Friday or the first time that the S&P 500 finishes the day in the green, whichever comes later.

Over three years of reporting for On the Edge, I witnessed Silicon Valley’s increasing support for Donald Trump, beginning with what was usually passed off as classically liberal support for free markets and free speech — values, I should mention, that I largely agree with — and culminating with Elon Musk’s endorsement of Trump following the assassination attempt against Trump last July.

You could say that Silicon Valley went “all in” in backing Trump — indeed, David Sacks, one of the hosts of the “All-In” podcast, is now the White House’s AI and crypto czar. But that isn’t really true. Silicon Valley isn’t a monolith, even though it’s subject to a particular sort of groupthink. Peter Thiel was a lone wolf when he endorsed Trump in 2016 — and although the Valley’s political attitudes have changed since then, it isn’t a complete transformation. Still now, there are plenty of “Silicon Valley types” who “like” tweets of mine that are critical of how Trump and Elon have conducted themselves during the first couple of months of the new administration. And if you surveyed the top founders and VCs, you’d find plenty who never boarded the Trump train.

However, the ones who got on board with Trump are often far more vocal than the dissenters. And in an industry where reputation is everything, the smoke signals that industry leaders send to one another matter. For instance, even Google CEO Sundar Pichai and Apple CEO Tim Cook attended Trump’s inauguration, while OpenAI CEO Sam Altman recanted his previous criticism of Trump. I have my doubts about whether any of these CEOs actually cast their ballots for Trump — instead, it was presumably a bottom-line decision. Altman’s tweet, for instance, came a day after Trump announced a joint venture that would invest in OpenAI and other companies.

Contrary to the New York Times, however, I don’t think it’s hard to explain why some voices in the Valley — including Musk, who has signaled his displeasure with Trump’s tariff policy in increasingly unsubtle ways and reportedly pushed him privately, too— are now having second thoughts. (Some of Trump’s backers on Wall Street also want “backsies”.) They were betting on, essentially, a replay of Trump’s first term. After years of feeling piqued by California’s leftward cultural swing and heavy tax and regulatory burdens, they thought they’d get on the right side of a conservative vibe shift. But they also thought they’d get a good economy, run on free market principles — or better still, one where they’d be dealt into an advantaged position because of Trump’s predictable cronyism.

Whether heartfelt or cynical, this willingness to play ball with Trump initially appeared to provide a strongly positive ROI. Shares in the top publicly-traded Silicon Valley firms — I’ll explain in a moment how I define that term — rose by 21 percent from the day before the election on Nov. 4, 2024 through their peak on Feb. 18, 2025, considerably outpacing major stock indices (including the NASDAQ, which also heavily weights many Silicon Valley firms). Since that peak through yesterday (Apr. 7), however — in barely more than six weeks — they’ve plunged by 27 percent, also more than the rest of the market.

Introducing the SV50 (Silicon Valley 50)

“Silicon Valley” is an ambiguous term because it both refers to a physical place — particularly Santa Clara and San Mateo Counties in California — and also (like “Hollywood” or “Wall Street”) serves as a metonym for the tech industry. Just as hedge funds in Connecticut are still considered a part of “Wall Street”, tech firms with headquarters in San Francisco, which the Valley itself has long had a love-hate relationship with, are a part of Silicon Valley for all intents.

Whether firms elsewhere on the West Coast qualify — like Amazon in Seattle and Microsoft in Redmond, Washington — is more debatable. Social ties and agglomeration effects matter a lot in Silicon Valley, enough that constant threats to flee the Bay over taxes or wokeness have largely been idle — although there are important exceptions, including Musk’s Tesla, which is now HQed in Austin.

So, I decided to create a stock index for Silicon Valley that might be compared to others like the NASDAQ or the S&P 500, which meets both of these definitions. To qualify, firms must be in tech or “tech-adjacent” industries and located somewhere in the nine counties of the Bay Area. So, for instance, the discount department store chain Ross Stores doesn’t qualify even though it’s headquartered in the East Bay because it has nothing to do with tech. But Amazon and Microsoft don’t qualify either up there in Seattle.

I did, however, decide to make exceptions for firms that have left California since 2020 but were founded in Silicon Valley. It would be strange to have a “Silicon Valley” stock index that doesn’t include Tesla or Thiel’s Palantir, for instance — and in recent years, the decision to relocate has often been correlated with Trump-friendly political attitudes. I also included two firms, Jack Dorsey’s Block (formerly Square) and Brian Armstrong’s Coinbase, that now claim to have no official HQ. Although not all Silicon Valley firms have embraced remote work, the declaration that you don’t have a physical HQ is also canonically Silicon Valley in its way.

These may not be exactly the 50 largest publicly-traded Silicon Valley firms by market capitalization2, but it should be pretty close. Note, however, that the “publicly-traded” qualifier is important. All major Silicon Valley VC firms are private. So are some of their more successful investments, such as OpenAI and Stripe — though outside of AI, we’re in a phase now where this was less true than it once was.

Firms are weighted in the SV50 by the natural logarithm of their market cap as of November 4, 2024 — the day before last year’s presidential election. But this relatively gentle weighting system doesn’t let the index get dominated by a small handful of firms. The largest companies — Apple, Alphabet (a.k.a. Google) and the semiconductor manufacturer Nvidia have a weight of 8 — while the smallest firms in the index have a weight of 3.

Here’s the list, including the performance of each stock since Nov. 4, 2024 — again, the last trading day before the election — and Jan. 17, 2025, the final day when public markets were open before Trump’s inauguration:

Since the election, 40 of the 50 firms have seen their share price decline. And since the inauguration, all but four of the 50 have lost value.

Of course, most American stocks have lost value during this period too, including many “Main Street” names, especially given the crash in the market since Trump’s “Liberation Day” announcement. But firms in the SV50 have particularly taken it on the chin: 37 of 50 have declined more than the Dow Jones Industrial Average since Inauguration Day, and two-thirds have fallen by more than the S&P 500.

Even as compared with the tech-heavy NASDAQ, which includes a lot of overlap with the SV50, you can see some decoupling. I’ve set the SV50 such that it had a value of 10,000 on Nov. 4 (and for purposes of the graphic you see above, recalibrated the major stock market indices to place them on the same scale). The SV50 peaked at a value of 12,103.96 on Feb. 18, which equates to its value rising by 21 percent just since the election. By contrast, the NASDAQ’s post-election gains peaked at about 11 percent. Investors initially agreed with the VCs and CEOs that Trump would be good for business. But since then, their prices have crashed.

The 3 forces behind Silicon Valley’s mindset

Give us a week or so here: we plan to create a landing page where we’ll update the SV50 daily, along with improved graphics and perhaps some other bells and whistles, like performance by subsector (e.g., consumer products versus semiconductors). For now, though, let me close with a comment on the three gravitational forces that can tug at Silicon Valley in different directions and produce what are sometimes sharp shifts in its mindset. Since the situation is fluid, I’ll keep this brief-ish.

1. Long time horizon. If there’s one truly admirable thing about Silicon Valley, it takes a long view when most people don’t. Investments are usually made at a time horizon of a decade or more, and cohorts of new investments are often expected to lose money in the short run. This can liberate startups from the pressures of publicly traded firms, with their focus on meeting quarterly earnings targets. And there’s a payoff for that: the evidence I gathered for my book suggests that the top Silicon Valley VC firms really do earn exceptionally high returns on investment that compound over time; this is why it has so much wealth and power now. (You can do the math yourself: an investment whose value compounds at a rate of 1.2x per year will be worth more than 6x your stake a decade later.) The long time horizon isn’t the sole reason for this; winner-take-all effects matter too. (The top Silicon Valley firms basically get to pick and choose the best founders from all around the world; the middle-tier VC firms don’t have particularly high returns, conversely.) But patience is generally at a premium in the United States, so having patience pays a premium.

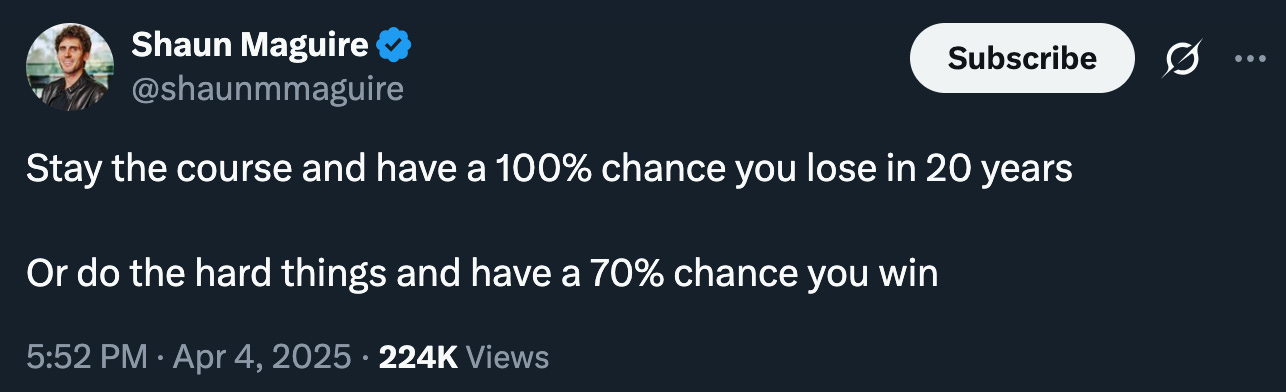

If you’re going to defend Trump’s tariffs, your argument basically has to revolve around some version of “short-term pain for long-term gain.” Now, I don’t think this is a good defense, particularly given the clumsy, brute-force nature by which the tariffs were implemented. But hey, I’m also not a macro guy. If you want to tell me that re-industrializing the American economy will work, and help the US to become more independent or reduce our debt levels at very long time frames, I have better things to argue with you about.3 Anyway, a defense like this one from Shaun Maguire, a partner at Sequoia Capital, is at least intellectually coherent:

What Maguire leaves unsaid is that there’s also virtually a 100% chance of pain in the near term. And in a political system where we hold elections every four years, it’s unusual for governments to adopt such positions. Even before “Liberation Day”, there were already signs of a backlash against Trump, and a tariff-induced recession — one that won’t just hurt the stock market but also produce considerably higher prices for consumer goods — would almost certainly accelerate one. Of course, such a backlash wouldn’t leave Silicon Valley unscathed either, particularly if the backlash takes on a more populist flavor.

2. Contrarianism. Silicon Valley may or may not embrace the “c-word” — contrarian — but it takes pride in thinking differently. Indeed, this is also a part of its investment strategy. Early-stage startups are typically in emerging industries that haven’t yet found a market but which will seek to do things — from space travel to creating artificial general intelligence — that would strike many people as ridiculous.4

This contrarian mindset can also translate into social and political attitudes. Like people in Silicon Valley, I share the view that the expert class is sometimes wrong, from the way the United States has handled foreign wars and COVID to our inability to build new things at a reasonable price.

But you have to be careful not to slip from acknowledging that the experts are sometimes wrong — in ways that may make for profitable investment opportunities — to believing that they’re always wrong. And many of the Silicon Valley types I spoke with for the book have trouble with this, particularly given that they feel like they’re on a winning streak, not just being fabulously rich5 but also having sussed out the conservative vibe shift and joined the Trump train at what they thought was just the right time. For a certain type of VC, the fact that “the experts” are almost unanimously against tariffs (at least in the way that Trump has implemented them) is actually viewed as an endorsement of the policy.

However, there are limits even to this extreme form of contrarianism. Silicon Valley can be remarkably “skilled” at denying discomforting, contradictory evidence — although so can all of us. But Silicon Valley is still grounded enough in reality that they’re looking at the stock market — indeed, the Valley (like Wall Street) tends to be big believers in markets. And VCs are also hearing from their founders, who have access to a lot of “ground truth” data like sales figures or recruitment pipelines.6

3. Herding and groupthink. The third major trait, which I also cover in the book, is that Silicon Valley investors often behave as a herd. There are several reasons for this. It’s a tight-knit community, with at most a few dozen VCs who really matter, mostly located in close geographical proximity. Furthermore, their interests are correlated — startups often receive funding from several VC firms between different investment rounds. Also, as was pointed out to me by Sebastian Mallaby, the author of the excellent book The Power Law, there’s not much “negging” in VC because there’s no good way to short a private company.7 So, Silicon Valley types tend not to criticize one another — in contrast to Wall Street types, whose trading strategies rely more on a zero-sum game where they seek to exploit the flaws in their competitors’ thinking to make bets.

Of course, you can see that attitude #2 (contrarianism) and attitude #3 (herding) are in some tension. They aren’t completely contradictory because VCs can be conformist relative to one another but contrarian as compared with the rest of society. Nonetheless, these combine to produce an equilibrium where Silicon Valley often moves in big sweeping arcs rather than rapid-twitch zig-zags like on Wall Street.

So if a cohort of important Silicon Valley leaders get into Trump, they’ll get really into Trump, riding the wave to the point where Elon even wears a hat saying “TRUMP WAS RIGHT ABOUT EVERYTHING”. And this can blind them not only to the devils in the details — which they’ll often write off as rounding errors8 — but also rather important considerations like that Trump consistently campaigned on tariffs. Even within Silicon Valley, Maguire is an outlier for defending the tariffs on the merits. Most of these guys were betting that Trump wasn’t serious — the same incorrect bet that Wall Street made — or that they’d be able to sweet-talk him out of it.

But when Silicon Valley does change course, it can be sweeping: a tidal shift, a preference cascade, one that might lead Silicon Valley to reconsider its other assumptions too, possibly including the wisdom of investors on the Tech Right relative to others in the Valley who kept Trump more at arm's-length. If the Trump bet were at least good for business, the optics around supporting Trump wouldn’t matter so much — but so far, it hasn’t been.

I weirdly even have a little bit of experience thinking about supply chains as my first job out of school was working as an economic consultant, helping multinational corporations to optimize their tax strategy for components that were manufactured at different places around the globe — granted, not God's work, exactly.

I broke what were essentially ties at the bottom of the list by some subjective factors, including a company’s recognizability and whether it’s listed in the S&P 500.

Although this is also a weird case to make if you think AI is going to transform everything anyway within 5 to 10 years. But see? There, I’m arguing when I said I wouldn’t.

Though I’d note here that many investments are in more boring categories like SaaS — Software as a Service.

Of course, there are significant survivorship effects here. A fledgling VC firm that makes a bunch of bad investments may never be heard from again.

Trump’s anti-immigration policies aren’t good for the industry either, and it’s noteworthy that skilled immigration is the one big fight that Musk picked with the right before tariffs.

If you think OpenAI is going to collapse under its own weight, for instance, you have to jump through a bunch of hoops to make what are, at best, loose proxies for that trade.

This attitude itself isn’t so bad — if you’re thinking in terms of scale, you want to worry about the problems that have a lot of 000000s attached — but that assumes you’re able to distinguish the more important details from the less important ones.

Once again having normal center-right to center-left politics would have given one the best model of reality. It was always extremely obvious that someone with the intellectual and character issues of Donald Trump would be a poor choice to steer the ship of state.

Who could have guessed that betting on the lying, idiotic, buffoon who's only out for himself wouldn't pay off?